Berachain Launches PoL Mining: Can $HONEY "Sticky" Liquidity in the Ecosystem?

Original Article Title: Berachain's Proof of Liquidity: Is It Sticky Though?

Original Article Author: Castle Labs, Web3 Ecosystem Partner

Original Article Translation: DeepSeek

Editor's Note: PoL requires staking assets in a liquidity pool rather than static locking, utilizing liquidity incentives, validator dynamics, and ecosystem optimization to improve capital efficiency, enhance network security, and DeFi liquidity. Currently, Berachain has a stablecoin APR of over 20%, and with the PoL launch, Berachain is expected to address DeFi inefficiencies and drive ecosystem growth. However, its success still faces challenges such as operational complexity, incentive misalignment, and regulatory uncertainty.

Below is the original content (slightly rephrased for clarity):

With the launch of PoL, can Berachain prove that its liquidity mechanism will fundamentally transform the DeFi landscape?

Berachain is an emerging Layer1 blockchain with a core design principle of leveraging Proof of Liquidity (PoL), a consensus mechanism that integrates liquidity provision into network security to empower value for ecosystem applications.

The system adopts a dual-token model ($BERA and $BGT) aimed at building a mutually beneficial ecosystem for validators, developers, and users (refer to the Honeypaper whitepaper).

With the PoL deployment, we will witness whether Berachain can address the inefficiencies in the DeFi space and meet market expectations.

Operation Mechanism of Proof of Liquidity

Unlike traditional Proof of Stake (PoS), PoL requires staked assets to be in a liquidity pool rather than static locking. This mechanism operates through the synergy of the following components:

1. Liquidity Incentives

Users who deposit assets into whitelisted DeFi protocols (such as DEX or lending markets) can receive $BGT from a reward treasury. These smart contract-controlled pools continuously release $BGT to incentivize users to enhance ecosystem liquidity.

Unlike transferable rewards, the non-transferable nature of $BGT ties its value to ongoing participation, promoting long-term commitment.

2. Validator Dynamics

Validators stake the network Gas token $BERA to maintain chain security and earn $BGT rewards. Their key obligation is to allocate a portion of the rewards to a designated treasury to guide liquidity toward specific applications. In return, validators may receive protocol fees or native tokens as incentives, forming a symbiotic relationship. This structure highlights PoL's emphasis on mutualistic benefits.

3. Ecosystem Synergy

PoL builds a triple-incentive system for validators, applications, and liquidity providers. The protocol boosts competition rewards for validators distributing $BGT, while users delegate their $BGT to preferred validators. This design of a quasi-resource allocation market achieves network-level optimization of capital efficiency.

4. Capital Efficiency and Security

Traditional PoS locks capital in staking contracts, whereas PoL enables staked assets to secure the network and provide DeFi liquidity simultaneously. If this dual-purpose design scales successfully, it could make Berachain a benchmark for a sustainable blockchain economy.

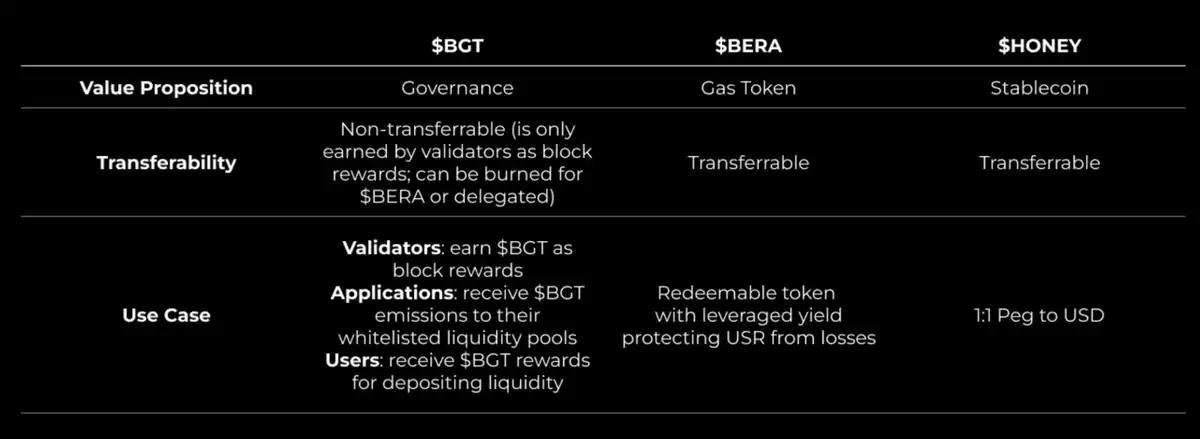

Tokenomics: Dual-Token System

According to the Honeypaper, the Berachain ecosystem is driven by two distinct utility tokens:

· $BERA: The native Gas token used to pay transaction fees and validator staking, serving as the cornerstone of network security and operational costs.

· $BGT (Governance Token): Liquidity providers acquire it through market-making, holders can burn $BGT at a 1:1 rate to receive $BERA, or influence reward distribution through delegation. Its non-transferability ensures governance remains in the hands of active participants.

This model establishes validators relying on $BERA for security and users guiding liquidity through $BGT, creating a positive feedback loop to drive ecosystem growth.

$BGT Liquidity Forecast and Ecosystem Impact

The success of PoL hinges on the distribution and use of $BGT. This section outlines its potential impact:

1. Liquidity Aggregation

$BGT is expected to flow into DEXs, lending protocols, and other high-yield platforms—areas that have long dominated DeFi transaction volume. Validators may prioritize treasury rewards, leading liquidity toward established use cases. However, with a well-designed incentive mechanism, emerging areas such as derivatives or RWAs also have opportunities.

2. Network Activity

Validators maintain blockchain security and earn $BGT rewards by staking the Gas token $BERA in the staking network. Their key responsibility is to allocate a portion of the $BGT issuance to a reward pool, effectively directing liquidity into specific applications. In return, validators receive income shares, native token rewards, and other diverse incentives—forming a symbiotic relationship. This architecture distinctly embodies the core pursuit of PoL (Proof of Liquidity) for mutual benefit and incentive alignment.

3. Ecosystem Expansion

The deep liquidity spawned by PoL attracts developers and capital influx. Blocmates analysis suggests that new projects, from yield aggregators to cross-chain bridges, may onboard, echoing the scenario of Polygon's ecosystem TVL growing by 300% in 18 months post-2021.

4. Validator Competition

Validators strategically allocate $BGT rewards to attract delegations. According to Berachain forum disclosures on the reward pool whitelist mechanism, protocols offering the optimal risk-adjusted return may dominate early liquidity trends, shaping the overall ecosystem development focus.

Opportunities and Risks

Opportunities

• Capital Efficiency Enhancement: The dual-purpose staking assets enable PoL's locked capital throughput to potentially exceed traditional PoS by 15-25%, significantly reducing opportunity costs compared to the Ethereum staking model

• Decentralization Resilience: The distributed distribution of rewards among validators, users, and applications helps mitigate centralization risks

• Long-Term Growth: A liquidity-driven security model can attract institutional-grade DeFi projects, supporting 3-5 years of ecosystem expansion

Risks

• Operational Complexity: The multi-layered mechanisms involving validator rewards, reward pool whitelist, and $BGT delegation may deter regular users, with the first-year adoption rate potentially reaching only 10-20% of the target audience

• Incentive Misalignment: Validator collusion with protocols can distort the flow of $BGT (as evidenced by early governance disputes in SushiSwap)

• Validator Reliance: Network stability hinges on validators surpassing short-term self-interest to pursue collective well-being—something hard to predict pre-mainnet launch

• Regulatory Changes: The integration design of liquidity tokens and governance tokens may face regulatory uncertainty in jurisdictions such as the United States regarding DeFi regulations

Summary

In the current sluggish market environment, Berachain's PoL launch can be considered one of the few highlights, injecting new excitement into the industry.

This is the first major test of its concept validation, which will determine whether PoL can truly open up a new paradigm. Although projects like Initia have had similar attempts with "built-in liquidity," Berachain is the first case to undergo a real test.

Will it be a success? Can the "honey" truly create highly sticky liquidity? The answer will soon be revealed!

Original article link: Link

You may also like

The impossible triangle is simply a pseudo problem

Stablecoins Finally Find Real Returns: On-Chain Reinsurance Re Explained | Interview with Re Founder Karan Saroya

The AI gamble of mining companies: Valuations enter a phase of differentiation, and it's hard to turn the tide

A letter from Alliance to entrepreneurs: Written on the occasion of Cursor selling for 60 billion dollars

Will MicroStrategy fall into a death spiral? What will the macro trend be in the second half of the year?

Blockchain Capital Partner: The Core Secret of Arbitrage

STRC unanchored by 11%, can the perpetual motion machine of Strategy still operate?

Bitcoin Market Analysis 2026: Can BTC Reach $150K by Year-End?

Bitcoin ETF Outflows Hit a Record $4.4 Billion: What Are Traders Doing With Their Cash?

WEEX App Just Got Smarter – New Tabs for Faster Trades & Easy Asset Management

WEEX All-New Search Features: Find, Trade & Earn Faster Than Ever

Morning Report | Illinois signs the strictest digital asset tax law in the U.S.; RWA tokenization market size surpasses $43 billion, institutions accelerate the migration of on-chain assets

Full version of the debut Q&A! Federal Reserve Chairman Waller: Sticking to the 2% inflation target, establishing five special working groups, individual did not submit the dot plot

From Disruptor to Shadow Market: The Crypto Market is Becoming a Colony of Traditional Finance

Dalio's important long article: How to position in the current market environment?

OKX Star analyzes Binance's competitive advantages: when regulation levels the playing field, competition has just begun

New gameplay for participating in initial offerings on cryptocurrency exchanges