Copycat ETF Applications Surge, Is the Era of ETF 2.0 Approaching?

After a high-profile announcement by Trump regarding a strategic reserve of cryptocurrency, traditional financial institutions were quick to react despite the lackluster market performance. Following the SEC's consecutive confirmations in February this year of several applications from American traditional giants for LTC, DOGE, SOL, and XRP ETFs, favorable policies and relaxed SEC regulations have led to frequent progress updates on Altcoin ETFs this week.

Latest Altcoins Applying for ETFs

The U.S. ETF application process follows this order: the issuer first submits S-1/S-3 forms, then the exchange submits a 19b-4 form, followed by a public comment period. The SEC then reviews and provides feedback, leading to final approval. The entire process typically takes around 6 to 8 months, depending on the SEC's review timeline. Below are the recent Altcoins applying for ETFs and their market performance data in the last 30 days, sorted by application submission date.

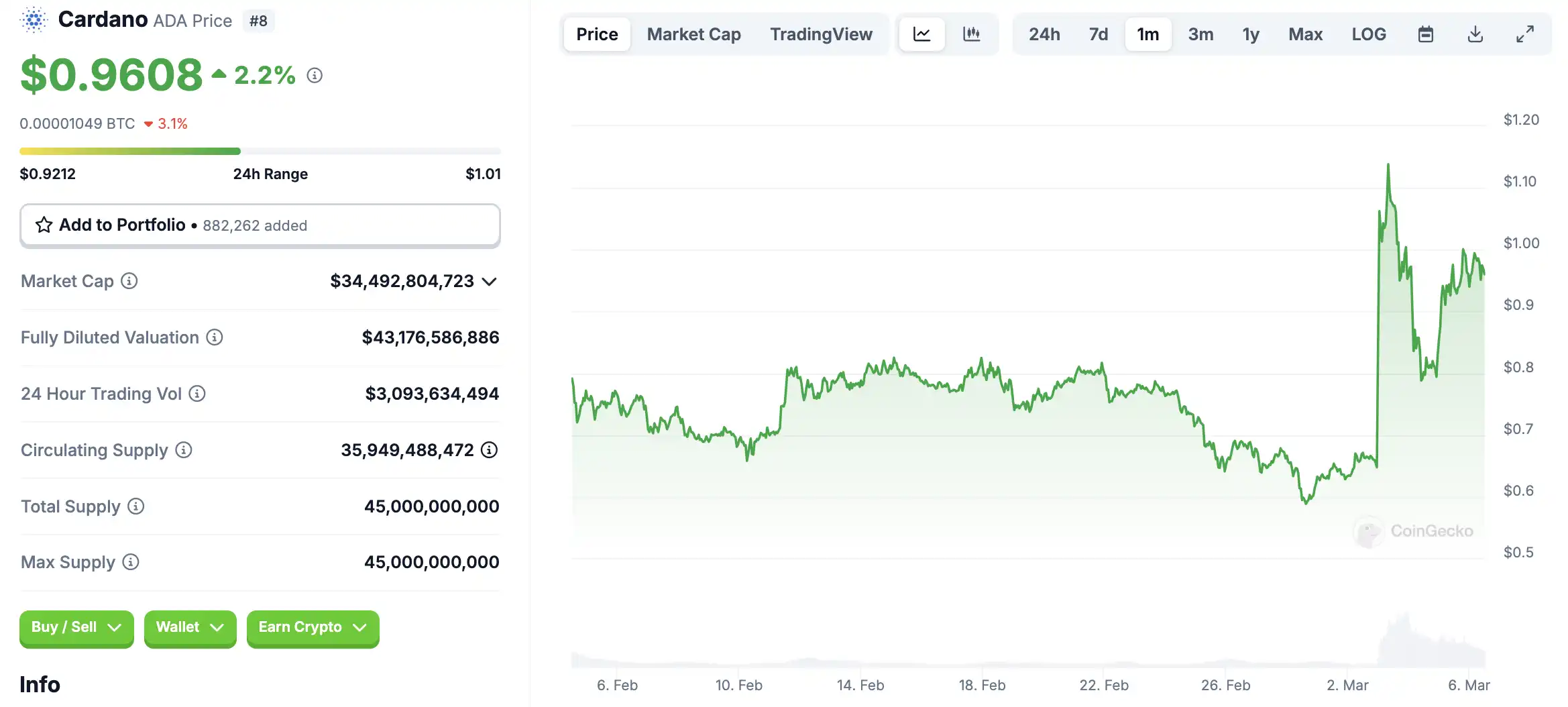

Cardano (ADA)

On February 25, the U.S. Securities and Exchange Commission (SEC) confirmed the acceptance of NYSE Arca's application, on behalf of Grayscale, for a spot Cardano (ADA) ETF. The application, submitted on February 10, will be custodied by Coinbase Custody Trust Company, with BNY Mellon handling asset servicing and administrative management.

On March 2, Trump made a social media post "pumping" ADA as part of his cryptocurrency strategic reserve, causing ADA to surge over 70% that day.

DOT (Polkadot)

On February 25, Nasdaq submitted a 19b-4 application for the Grayscale DOT ETF (Grayscale Polkadot Trust).

HBAR (Hedera)

On February 24, Nasdaq filed a 19b-4 application with the SEC for HBAR ETF by Canadian investment firm Canary Capital; on March 4, Nasdaq filed a 19b-4 application for Grayscale's Hedera ETF.

Hedera is often seen as a cryptocurrency dark horse. The most anticipated aspect of Hedera is the possibility of a spot HBAR ETF going live, with Valour Funds having submitted an application for a physically backed product on the Euronext exchange in Europe. Meanwhile, Canary Capital has filed an application for a US-based spot HBAR ETF, further raising market expectations as investors closely watch regulatory developments in the post-election environment.

AXL (Axelar)

On March 6, Canary filed an S-1 application for its AXL ETF.

Additionally, former Coinbase Chief Legal Officer Brian Brooks has joined Axelar's new Institutional Advisory Council, focusing on regulatory coordination and institutional adoption.

As previously reported by BlockBeats, Canary Capital has launched the AXL (Axelar) Trust, which will hold the native tokens of the Axelar network, making it the first investment trust to offer exposure to a general-purpose blockchain interoperability protocol.

This trust will provide institutional investors with an opportunity to invest in blockchain interoperability technology, connecting to the Web3 ecosystem, including XRP Ledger, Hedera, Stellar, TON, Sui, Solana, and Bitcoin.

APT (Aptos)

On March 6, Bitwise formally filed an S-1 application with the SEC to register a potential Aptos ETF, taking the first step towards launching an Aptos ETF in the US market.

Aptos is in collaboration with major asset management firms to launch a US-listed ETF, making it one of the few global crypto protocols to achieve this milestone.

Prior to this, Bitwise had already launched the Aptos Staking ETP on the Swiss Stock Exchange in November 2024, allowing for staking of the Aptos token.

How Has the Ethereum ETF Performed Since Approval?

The Ethereum ETF officially debuted on the U.S. capital market on July 23 of last year, with the price of Ethereum around $3200 on that day. Market data shows that the net inflow into the Ethereum ETF in the past six months has been $2.76 billion, equivalent to Wall Street purchasing nearly 1% of Ethereum's volume, while Ethereum's price has now dropped to around $2500.

This is partly due to Grayscale continuously selling off the Ethereum ETF, becoming the market's largest seller, hindering Ethereum's price rise; on the other hand, Ethereum is more severely affected by whale selling pressure compared to Bitcoin, and Ethereum is currently absorbing the potential selling pressure from whales.

However, the good news is that entities related to Trump, such as World Finance Liberty, are continuously increasing their holdings of Ethereum. The net inflow of the ETF and continuous purchases by Trump-related institutions demonstrate the attitude of long-term investors towards Ethereum in an increasingly open policy market environment.

By extension, if the aforementioned altcoin ETFs are approved in 2025, although ETFs in this category will become an inflow window for traditional funds, it does not mean that these tokens will experience a significant upward trend.

Crypto ETF 2.0 Under the Trump Administration

Looking at the history of crypto ETFs, it is easy to see the significant bullishness on the market as a whole following Trump's return to the White House this year. Bloomberg analyst Eric Balchunas pointed out that before Trump won the election, the approval probability of all assets, except for Litecoin, remained below 5%. It is expected that as the applications enter the approval process and the SEC's decision deadline approaches, the approval probability of cryptocurrency ETFs will continue to rise.

Related Reading: "Coinbase 2025 Outlook: More Crypto ETFs to Come; Stablecoins Still a 'Killer App'"

What Impact Does This Have on the Crypto Market?

Bloomberg analysts expect the SEC to make a decision on the proposed altcoin ETF in October this year. It is foreseeable that if the altcoin ETFs are approved consecutively, future bullish news is likely to continue attracting more conservative and institutional investors, thereby altering the market's investor structure. In this policy environment, the crypto market may experience enhanced liquidity, price surges, and changes in investor structure. Therefore, the approval of more ETF products is also expected to bring more funds into the crypto market, enhance market liquidity, and thus reduce price volatility.

Furthermore, due to regulatory arbitrage, ETFs introduced in the United States may directly trigger imitation in other countries and regions worldwide. This imitation may to varying degrees drive the global adoption of cryptocurrencies, especially in regions with relatively lenient regulations, where cryptocurrency adoption could see accelerated growth. Global policy convergence can not only effectively reduce compliance costs for cross-border transactions but also further eliminate investors' concerns about legal risks, thereby promoting more institutional and individual participation. This trend may accelerate the transition of cryptocurrencies from fringe assets to mainstream financial instruments, boosting their status in the global economy.

As the Trump administration further supports the crypto industry, U.S. states are gradually introducing "Strategic Bitcoin Reserve" legislation, combined with the Republican control of both houses of Congress, there may be an opportunity for Congress to pass cryptocurrency-related bills. Once the legislation is passed, cryptocurrencies may have the opportunity to become a new asset class that is neither a security nor a commodity, which would be groundbreaking for the crypto market.

Which Altcoins Could Apply for an ETF?

As the Trump administration continues to loosen crypto regulations, 2025 could see a peak in applications for altcoin ETFs. Some institutions have predicted that the surge in demand for cryptocurrency ETFs will surpass precious metal ETFs in total assets in North America, becoming the third-largest asset class in the rapidly growing $15 trillion ETF industry, second only to stocks and bonds.

Especially for altcoins highly relevant to the U.S., they are more likely to be favored. For example, ONDO (Ondo Finance), as a representative of the RWA track anchoring real-world assets like U.S. bonds, may be the first to receive approval for a tokenized government bond ETF and even become a core target for traditional institutions to allocate crypto assets. If the FIT21 bill is passed within the year, establishing the "Decentralized Protocol Securities Law Exemption" principle, mainstream U.S. DeFi tokens such as UNI (Uniswap), MKR (MakerDAO), AAVE (Aave), etc., may accelerate integration into the traditional financial system.

You may also like

Will MicroStrategy fall into a death spiral? What will the macro trend be in the second half of the year?

Morning Report | Illinois signs the strictest digital asset tax law in the U.S.; RWA tokenization market size surpasses $43 billion, institutions accelerate the migration of on-chain assets

Full version of the debut Q&A! Federal Reserve Chairman Waller: Sticking to the 2% inflation target, establishing five special working groups, individual did not submit the dot plot

From Disruptor to Shadow Market: The Crypto Market is Becoming a Colony of Traditional Finance

Dalio's important long article: How to position in the current market environment?

OKX Star analyzes Binance's competitive advantages: when regulation levels the playing field, competition has just begun

New gameplay for participating in initial offerings on cryptocurrency exchanges

Why Is Bitcoin Down Today? What the Hawkish FOMC Means for SpaceX, Gold and Nasdaq

DeepSeek Financing Story

Morning Report | DeepSeek completes over $7 billion in financing, with a valuation exceeding $50 billion; Musk's personal wealth has surpassed the total market value of Bitcoin

Cursor, why did you get on Musk's spaceship?

In the name of charity, for the benefit of the family: How the Trump family turned charity into profit?

Will Gold Break $4,500 After Tonight's Fed Decision? What XAUT and PAXG Traders Need to Know

SharpLink CEO: How to understand that Ethereum developers have just surpassed 1 million?

Morning Report | MiCA grace period expires on July 1; Kalshi's trading volume in the first week of the World Cup breaks $5.1 billion, setting a record

The foundation of SpaceX's trillion-dollar valuation: Who is dividing Musk's annual capital expenditure of tens of billions?

How to exit after asset tokenization?