Go Left? Go Right? The Crossroads of Cryptocurrency

The recent Libra incident has completely exposed the dark side of Crypto, once again fulfilling Plato's Allegory of the Cave. Even on the most transparent blockchain, we can only catch a glimpse of the shadows cast by the torches outside the cave. However, this Libra incident unprecedentedly revealed the outside scene to those inside the cave, creating a complex situation involving central aspects of national power, market makers, the core DeFi project on Solana, and key players in the industry.

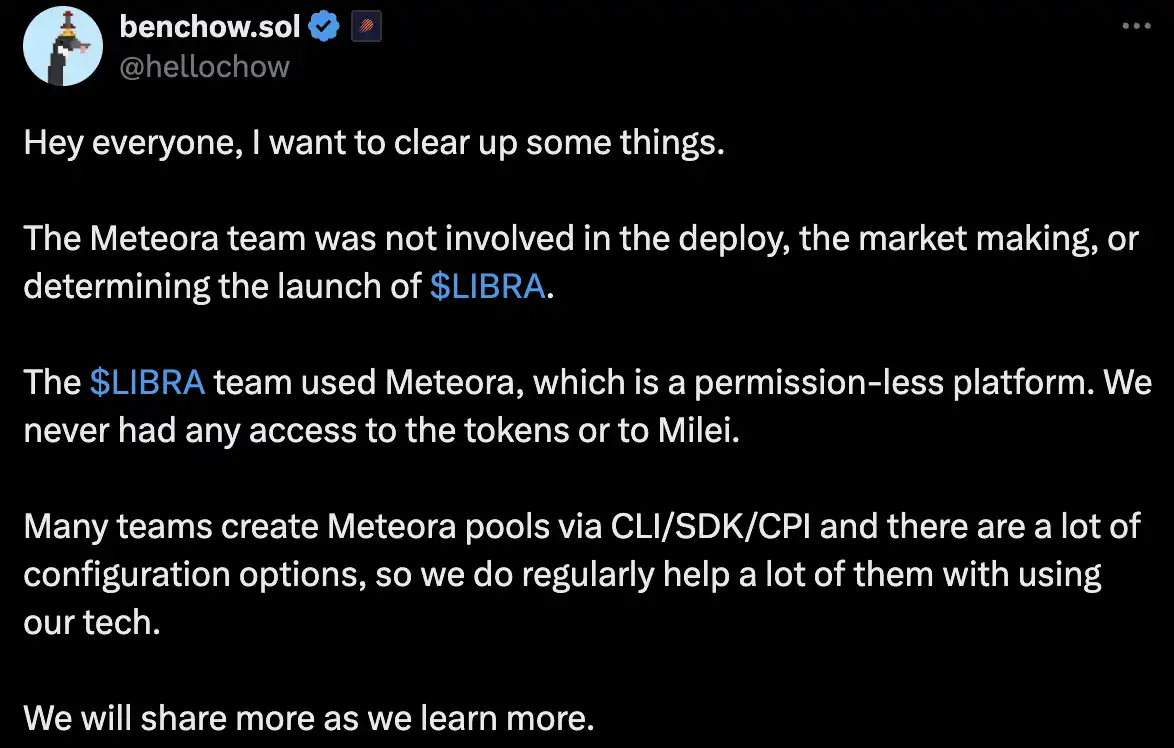

After the event, it left behind many issues that the entire industry needs to address. Among them, Solana's core DEX, Jupiter, and Meteora were embroiled in the center of the whirlpool of this event. The joint statement released by BenChow, the co-founder of both projects, prompted a rethinking of a long-standing issue in the blockchain space—the debate between "permissioned" and "permissionless" blockchain projects, representing the two factions of blockchain. In light of this, Dapenti BlockBeats invited dForce's founder, MinDao, to discuss the reflections behind this event.

The Boundaries of "Permission"

As Jupiter and Meteora were deeply embroiled in confusion, social media was filled with discussions about their involvement in this event. DForce's founder, MinDao, stated, "The focus of the event is not on sniping but on using insider information to preemptively know about the authenticity of such events and then snipe. I don't understand why Libra chose to make such a complex setup through Meteora instead of easily issuing tokens using Uniswap."

When Ben pointed out that Meteora's DLMM pool required manual customization, the market naturally compared it to Uniswap V3's concentrated liquidity feature. The timeline goes back to the iconic vote initiated by Vitalik in 2018—over 80% of users supported "Uniswap should list freely," driving the blockchain from the ICO era to the DeFi permissionless era. Leveraging this mechanism, Uniswap once held over 80% of the DeFi market share at its peak, and its "permissionless" underlying logic still profoundly influences the industry's DeFi standards today.

During the same period of Uniswap's market dominance, Meteora quickly emerged as a prominent player in the Solana ecosystem after its launch. This was the time of DeFi Summer when all the stars aligned. However, Meteora effectively solved the slippage issue with its innovative routing algorithm, gaining a share of the DeFi market. After the team split off to create the aggregator Jupiter, the Jupiter ecosystem quickly surged ahead in market share, at one point occupying over 70% of Solana's liquidity inflows, becoming the most dominant entry infrastructure during Solana's DeFi tech boom.

Both are single-sided liquidity pools, one being the undisputed giant of the DeFi golden age, Uniswap, and the other being Jupiter, a grassroots-born underdog that rose to prominence. Despite Uniswap's 5-year history, enduring multiple bull and bear cycles, and launching countless rug tokens, it has not faced the same level of public outcry as Jupiter did in this incident. The reason behind this lies in a battle between open-source and closed-source.

Open Source or Closed Source? Ethereum or Solana?

Uniswap V3 enforces liquidity rules through mathematical formulas, with all parameters like fees and price ranges being publicly transparent and immutable. Therefore, even with single-sided liquidity, on-chain arbitrageurs can actively monitor on-chain data and conduct arbitrage to rebalance the market in real-time. This presents a high opportunity cost for projects expecting to control the market through partial price range manipulation. On the contrary, for DLMM, the project team needs Meteora's assistance to create a customized liquidity pool, a process that involves subjective judgments ("only Meteora can determine the reliability of the project team") and information asymmetry. For example, the Libra team may, under the guise of "enhancing user experience," request uncommon slippage parameters within special ranges or conceal liquidity lockup periods. These details often make it difficult for on-chain arbitrageurs to execute strategies quickly, leading to market price imbalances.

Related Reading: "Quickly Understand Meteora's Liquidity Price Range Viewing Method"

Meanwhile, the closed-source protocol and special liquidity pool settings allow celebrity tokens like $Libra to exit liquidity with ease and low risk when using Meteora DLMM. This indirectly enables teams behind malicious tokens to selectively harvest profits. According to Nansen's post-incident analysis report, among the 15,000 wallets with a PNL exceeding $1,000, 86.07% suffered losses totaling $250 million, while the remaining 2,100 wallets made profits of $180 million. Hayden, the founder of the main LP in this incident, KelsierVentures, openly stated that he profited $100 million from the trades and additionally received over $10 million in transaction fees.

In fact, even in cases where the ecosystem cannot be open-sourced or for products that require customization, there are multiple ways to avoid malicious behavior from behind-the-scenes market makers. Olympus Pro's Bond mechanism "Market Maker Collateral Requirement to Prevent Malfeasance" and Trader Joe's liquidity ledger with a time-weighted exit model "Unlocking in stages based on trading volume and survival time" can both cater to the needs of large-scale token launches and customization while protecting users.

The rapid rise of DLMM TVL post-Trump event, data from DeFiLlama

「There is no middle ground in permissionless DeFi or in running a compliant CEX」 MinDao also pinpointed the core of this, adding, 「Where is the boundary, what kind of product is called DeFi, I think we need a clear framework on this. I feel that everyone in the crypto circle is also looking for various compromises, striving towards a balance of compliance and decentralization.」

Indeed, as long as humans are involved in the process, it cannot be called DeFi "decentralized" finance, and this product will inevitably face regulatory compliance issues. Faced with this issue, even Uniswap Labs, which is completely separate from the protocol and the company entity, could not escape. The U.S. SEC once attempted to charge Uniswap Labs with operating an unregistered broker, exchange, and clearinghouse, and issuing unregistered securities. From warnings, sending a Wells Notice, investigation, to formal charges, Uniswap underwent a 3-year-long self-certification process with the SEC, forcing the team to waste a significant amount of time and millions of dollars until now, on February 26, 2025, the U.S. SEC finally dropped its investigation into Uniswap Labs. We are in a phase where traditional financial rules are being abandoned to regulate DeFi by force, and in the midst of upcoming DeFi regulations.

The Double-Edged Sword of Liquidity

The above-mentioned artificial "permission" risk is just one of the reasons for community opposition, and Meteora itself does not hold a significant market share and cannot shake the entire industry. What is truly concerning is the vertical dominance of the Jupiter ecosystem.

According to Dune data, Meteora's market share is only 5%

Starting in 2024, Jupiter began acquiring various ecosystem projects, from the user entry point Ultimate Wallet, to data analysis tool Coinhall, blockchain explorer SolanaFM, from the backend liquidity pool Meteora to the frontend Moonshot. By integrating wallet, data, and trading core infrastructure, Jupiter is building a self-contained DeFi service collection. Users can complete the entire process from depositing, trading to yield optimization within this ecosystem, and the recent launch of Jupnet indicates its intention to expand beyond Solana into the entire chain's DeFi ecosystem.

Such a powerful impact and product are like a double-edged sword. When nothing goes wrong, this is undoubtedly the best path for new users to enter the blockchain Mass Adoption, as seen from the potential demonstrated by the hundreds of thousands of non-crypto users added during the Moonshot to Trump Coin era. However, when it gets involved in an "insider trading" event, the market naturally becomes anxious about how to accept regulation for such a complex DeFi functionality and process, especially since it is tied to Solana, which currently has the largest liquidity in Crypto.

Just like the saying "everyone in the crypto world is making all sorts of compromises," the open-source Uniswap, for its own business logic, has set the shackles of the BSL "Business Source License" on V3 and V4 or has delisted some tokens from the frontend for regulatory legalization. How will the closed-source Jupiter compromise its own business blueprint and the balance between user trust and compliance?

Cultural DNA

When we extend the discussion to Uniswap and Jupiter, discussing whether ETH and Solana products have been influenced by the underlying culture of these two chains, MinDao believes that "Solana's closed-source pragmatism, pursuit of efficiency and value chain integration, is conducive to rapid expansion; while Ethereum's open-source freedom and diverse ecosystem require more considerations for development direction, and the underlying culture of the chain will profoundly influence the product's path."

In his article "Layer 2s as cultural extensions of Ethereum," Vitalik mentioned that Ethereum's underlying subculture is broadly divided into three camps: Crypto Punks, Regens, and Degens. Looking at it now, Ethereum's "crypto punk culture" is more vibrant, while the Degen culture has flourished in Solana. Ethereum leans more towards the white left, with its cultural DNA rooted in the spirit of open source and decentralized idealism, which is essentially a continuation of the BTC spirit, and its ecosystem evolution follows the logic of "common cooperation."

Ethereum core protocols like Uniswap and Aave are completely open source, allowing any developer to fork and iterate, as seen with Sushiswap forking Uniswap, forming a free-market competition. This has also led to the emergence of more niche products on Ethereum, each product excelling in its own field, with the product's moat being the "brand" itself. The speed of iteration and the solidity of the community significantly influence the project's dominance, while its development path is more horizontal.

Protocols on the EVM are mostly multichain

While Solana embraces efficiency, its culture is based on a competitive sports spirit and relentless execution, closer to Web2's "winner-takes-all" mentality. This has allowed the "Degen culture" to take root extensively in this environment. The Solana Foundation excels in proactively integrating resources such as capital and government relations, enabling them to develop at an extraordinary pace. This mindset has permeated various products on the platform, where most mainstream projects on Solana are either difficult to integrate with other chains due to the underlying technology, or choose to keep their source code closed to prevent on-chain competitors from copying them. Solana is adept at leveraging various resources to develop and prioritize creating a value chain with the highest efficiency, monopolizing the entire value chain, and controlling the interest chain, similar to Tencent's "super-app" strategy. For example, Jupiter has acquired Meteora (DEX) and Moonshot (fiat gateway) to achieve "trade-mint-liquidity," or more recently, Pumpfun announced the abandonment of Raydium to directly launch a product business adding AMM pools on Pumpfun.

Protocols on Solana are mostly single-chain

The Future of Blockchain, Ethereum to the Left, Solana to the Right

The "Liberal" Ethereum

The underlying cultures of both sides have also shaped the paths they are currently on. Firstly, environmentalist Vitalik proposed transitioning Ethereum from PoW (Proof of Work) to PoS (Proof of Stake) due to the excessive energy consumption of PoW. In September 2022, Ethereum completed The Merge, officially transitioning from PoW to PoS. Energy consumption decreased from approximately 78 TWh per year, equivalent to Chile's national electricity consumption, to about 0.01 TWh. The PoS-introduced staking mechanism with a "32 ETH threshold" and the deflationary model of EIP-1559's burning mechanism have transformed Ethereum's tokenomics. Post-merge, the circulating ETH supply decreased by 3 million, the annual inflation rate dropped from 3.5% to -0.2%, and the number of validator nodes expanded from a few thousand miners in the PoW era to over 1 million stakers.

However, this initial choice has led to a phenomenon where the PoS staking threshold of "32 ETH" restricts the participation of most ordinary users. The top three staking service providers—Lido, Coinbase, and Kraken—control over 35% of the staked amount, sparking criticisms of the market becoming "the richer getting richer." Even Ethereum core developer Dankrad Feist acknowledged that "if Lido's share exceeds 33%, it may trigger social consensus intervention." Coupled with the exorbitant GasFee, this has led to "whales" becoming the primary users of Ethereum, leading to Ethereum being known as a "noble chain."

The Ethereum Improvement Proposal (EIP) voting process is lengthy, and community consensus is difficult to quickly achieve unless driven by core members. Reports have indicated that 68% of Ethereum Improvement Proposals are implemented by 10 individuals associated with the Ethereum Foundation. However, ecosystem decision-making often gets caught up in multi-party games, leading to low efficiency in key upgrades. For example, innovations like "account abstraction" have not been fully deployed yet, and the transition to Proof of Stake (PoS) mentioned above has been ongoing for 6 years. The complementary "EIP-1559" fee burning mechanism took two years of discussion to be implemented. YBB Capital researcher Zeke believes that the EIP process has lost its original democratic intent: "Governance tokens are meaningless until the Sybil problem is solved. Democratic voting can never be reflected in proposal governance. In the current Ethereum ecosystem, similar to big institutions like a16z, a few wallets can veto a large community's approval votes, rendering the vote meaningless."

On the same day Trump announced strong support for the "American" blockchain, Vitalik tweeted that the Ethereum Foundation will avoid including: promoting any ideology, actively lobbying regulatory bodies and powerful political figures, especially in the United States or any major country, risking damaging Ethereum's status as a globally neutral platform, becoming an arena for vested interests, and becoming a highly centralized organization. Vitalik still hopes to maintain Ethereum as a digital Tower of Babel against authoritarianism, guarded by a globally open network of validators using mathematics.

The "Pragmatic" Solana

Image Source: Blockworks

In contrast, Solana, heading to the right, has gradually turned its vision of Mass Adoption through ultra-fast transaction efficiency and throughput into a reality. It has established overwhelming superiority in a blockchain, from transaction volume and activity to liquidity, making Solana a well-deserved leader. The launch of the Trump Coin can be seen as the best stress test of Solana's performance. $5.6 billion in real value was generated in a day, and half of the value was generated by outsiders who had never participated in blockchain. Polygon co-founder Brendan Farmer, however, expressed concerns about Solana's structural issues. Most of Solana's economic value is derived from pump and trading bots, forming a derivative industry of Meme coins that does not create any economic value. The consequence is that they will extract liquidity from the ecosystem. Each dollar of REV paid means a reduction in funds for future Meme coin transactions, creating a vicious cycle.

Over the past five years, Solana has experienced a total of seven independent outage events, five of which were caused by client errors and two due to the network's inability to handle a large volume of spam transactions. However, some community leaders, including Helius founder Mert Mumtaz, predict that outages will continue to occur. The exposed issue of Solana's excessive centralization was widely discussed around 2022, but as the market sentiment shifted from geek culture to an application-centric mindset, with Solana demonstrating transaction throughput comparable to Web2 networks, this issue has been of little concern to most.

Source: Helius Report on Solana Outage History

Unlike Vitalik, Lily Liu, the head of the Solana Foundation, mentioned in an interview, "We believe the new administration will recognize the role of blockchain in supporting the U.S. strategy, so we are very hopeful and have plans to collaborate with the U.S. government in the future." The Solana Foundation's excellent resource integration capabilities have shown that in this round of the market, opportunities have leaned towards Solana, from government support to even the U.S. president endorsing a memecoin. However, MinDao believes, "If Solana is too politically inclined, its politically interventionist nature will make it potentially vulnerable to political influences in the future globalized ecosystem. For example, if a Chinese company wants to issue a Layer2, they probably won't want to issue it on a chain that represents the U.S."

The Crossroads of Progress, Forward We Go

We are wandering between crossroads of left and right, seemingly facing a deadlock in Ethereum's governance gridlock and Solana's capital frenzy. However, this evolution movement that seems to "betray" its original intention may be forging the Holy Grail of a financial system that can accommodate both Hayek and Keynes.

Going left, Ethereum, after transitioning to PoS to reduce resource consumption and decrease the possibility of centralized regulation, has turned ETH into a chain for the elites. The initial intention to accept democratic voting through the EIP process has made Ethereum struggle. The ethos of being firm not to be involved in politics has also led it to lose to Solana in this round of large-scale application cycles. Even in 2024, Solana has surpassed Ethereum in ecosystem developer growth, despite Ethereum's status as a concentrated hub for ecosystem development.

The right-leaning Solana, with its high performance and cost efficiency, has rightfully become the "Liquidity King" amidst the Meme craze. However, by emitting hundreds of thousands of Meme tokens monthly, it has transformed Solana, originally envisioned as the decentralized "Nasdaq," into a perfect decentralized "casino." This situation simultaneously devours the potential value Solana could create in the future. Excessive involvement in geopolitics also limits its application on a global scale.

It seems that whichever path is taken, challenges are encountered.

Yet, MinDao remains optimistic about the left and right leanings towards "Ethereum" and "Solana." He believes that the competition between them is not a zero-sum game. The ultimate potential of blockchain is neither Ethereum's ideal state nor Solana's efficiency empire but a new species born through the confrontation and integration of both. This will undoubtedly include utilitarianism and perfect "decentralization" through a mechanism driven by economies of scale. This revolution is not a betrayal but a redefinition of the "revolution" itself.

Regarding the future path, Vitalik recently provided an answer in a Tako AMA, stating that it is no longer the era of infrastructure but the era of applications. Therefore, these stories cannot be abstract concepts like "freedom, openness, censorship resistance," etc. They require some clear application layer solutions. He proposed the concept of Ethereum as the world's finance and that it will further support application layer products such as info finance, AI + crypto, high-quality public goods financing methods, RWA, etc. Interestingly, the two factions represented by ETH and Solana are becoming more alike in their development process, akin to the obverse and reverse of a coin, the double helix of DNA. Only by transforming human game theory into a verifiable public knowledge core can blockchain evolve into a trustworthy value network.

a16z partner Chris Dixon believes that AI, the Internet, and Crypto all have their ups and downs. When we wait for things to improve before taking action, we find ourselves doing the same things as a large group. Thus, when people believe that a technology has reached its limit, it often conceals the best opportunities.

We are currently at a crossroads both horizontally and vertically. Whether we lean "left" or "right," the ultimate result will be moving forward. Perhaps the ultimate form of blockchain is neither the utopia of the "savior faction" nor the hegemony empire of the "apocalypse faction" but a hybrid that finds a dynamic balance between openness and efficiency, idealism and realism. The future belongs to those who can embed "imperfect human nature" in code yet maintain the system's robustness.

You may also like

Morning Report | Illinois signs the strictest digital asset tax law in the U.S.; RWA tokenization market size surpasses $43 billion, institutions accelerate the migration of on-chain assets

Full version of the debut Q&A! Federal Reserve Chairman Waller: Sticking to the 2% inflation target, establishing five special working groups, individual did not submit the dot plot

From Disruptor to Shadow Market: The Crypto Market is Becoming a Colony of Traditional Finance

Dalio's important long article: How to position in the current market environment?

OKX Star analyzes Binance's competitive advantages: when regulation levels the playing field, competition has just begun

New gameplay for participating in initial offerings on cryptocurrency exchanges

Why Is Bitcoin Down Today? What the Hawkish FOMC Means for SpaceX, Gold and Nasdaq

DeepSeek Financing Story

Morning Report | DeepSeek completes over $7 billion in financing, with a valuation exceeding $50 billion; Musk's personal wealth has surpassed the total market value of Bitcoin

Cursor, why did you get on Musk's spaceship?

In the name of charity, for the benefit of the family: How the Trump family turned charity into profit?

Will Gold Break $4,500 After Tonight's Fed Decision? What XAUT and PAXG Traders Need to Know

SharpLink CEO: How to understand that Ethereum developers have just surpassed 1 million?

Morning Report | MiCA grace period expires on July 1; Kalshi's trading volume in the first week of the World Cup breaks $5.1 billion, setting a record

The foundation of SpaceX's trillion-dollar valuation: Who is dividing Musk's annual capital expenditure of tens of billions?

How to exit after asset tokenization?

The stablecoin positioning battle escalates: When compliance is just a ticket to entry, will USD1 become the biggest winner?