Interpreting the AAVE Buyback Proposal: Is DeFi Finally Embracing Dividends?

On March 4th, Aave DAO service provider Marc Zeller released a governance proposal seeking governance approval for the formal Aave Request for Final Comments (ARFC), aimed at reshaping Aave's economic model. It is not a simple adjustment to the existing mechanism but a fundamental upgrade involving revenue distribution, incentive mechanisms, and long-term stability optimization.

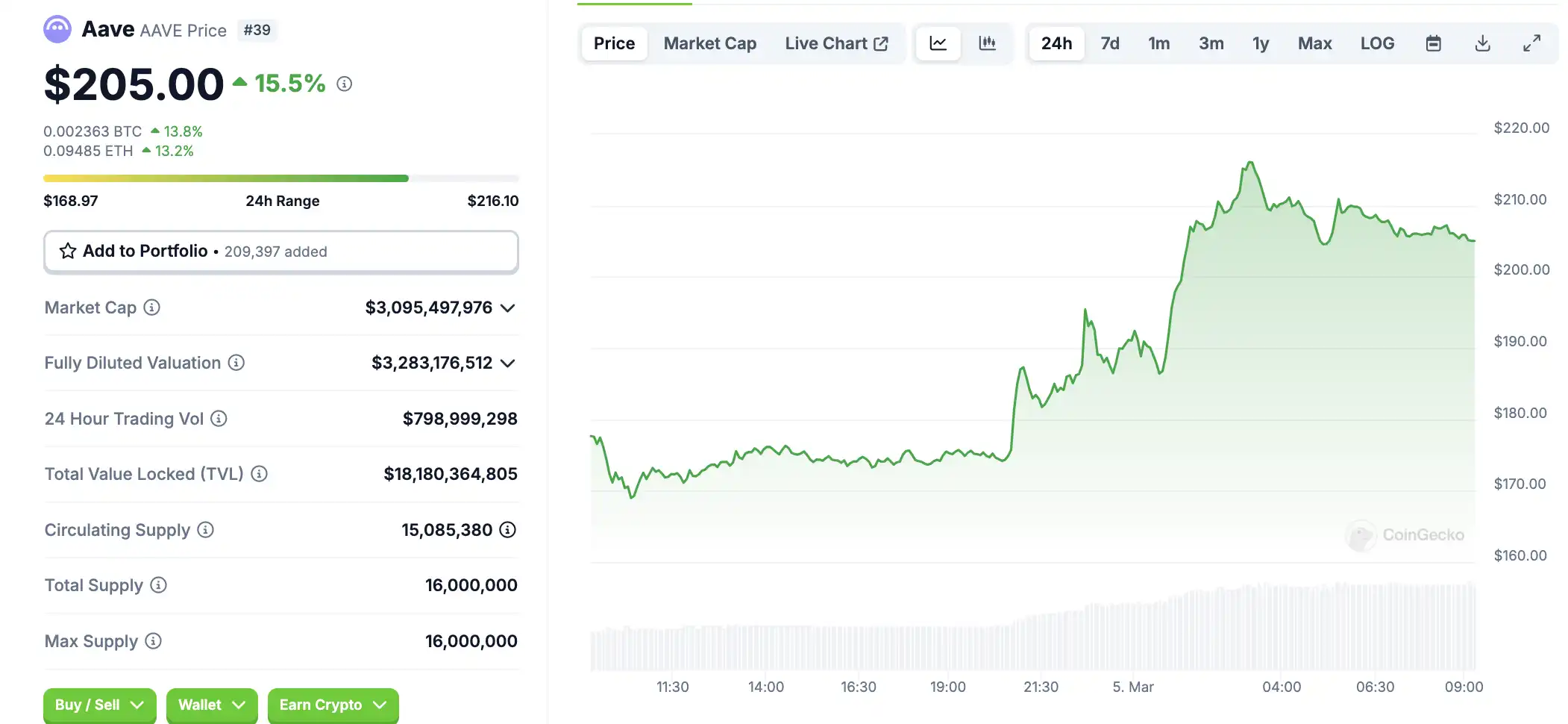

The proposal has currently only released the first part and is currently in the consultation phase. Since the proposal's release, the AAVE token has risen to a high of $216, with the current AAVE price at $215, marking a 15.5% increase in the last 24 hours.

Interpretation of Proposal Contents

Marc Zeller bluntly stated on X that this is the "most important proposal in Aave's history," illustrating its significant impact. The core pillars of the proposal include:

1. Revenue Redistribution Mechanism

2. AAVE Token Buyback and Distribution Plan

3. Umbrella Security Mechanism

4. LEND Token Retirement

According to the proposal contents, Aave has continuously expanded its market presence over the past two years, building a solid financial foundation.

Despite market fluctuations, Aave has maintained strong revenue growth, with the DeFi protocol's TVL increasing by 115% to reach $115 million. The robust financial position has enabled Aave to drive the tokenomics upgrade while remaining competitive.

Establishment of Aave Finance Committee

One of the core aspects of the proposal is the establishment of the Aave Finance Committee (AFC), which will serve as a key entity within the Aave governance framework, fully responsible for managing Aave's treasury and liquidity strategy. The formation of the AFC signifies Aave's progression towards a more professional and transparent financial management approach.

The main responsibilities of the AFC include overseeing all financial allocations within the Aave ecosystem, ensuring funds are used reasonably and efficiently, and achieving sustainable revenue growth. Additionally, it will develop and execute Aave's liquidity strategies to ensure the protocol maintains adequate liquidity under various market conditions. Most importantly, the AFC will be responsible for assessing and managing various financial risks faced by the Aave protocol, including market, credit, and operational risks.

In order to ensure the professionalism and effectiveness of the AFC, the committee will be supported by core stakeholders including Chaos Labs, TokenLogic, Llamarisk, and ACI. These institutions have a wealth of experience and expertise in the DeFi field and will provide strong support for AFC's decision-making.

Benefiting Stakers, Aave's Revenue Sharing Mechanism

The most eye-catching aspect of this proposal is the significant adjustment to the protocol's revenue distribution mechanism. Aave plans to allocate a portion of the protocol's generated revenue to stkAAVE stakers, more directly linking the protocol's success to the interests of AAVE token holders.

Specifically, Aave plans to introduce a "Fee Switch" mechanism. This mechanism will allow Aave to release excess protocol-generated revenue (such as lending fees) from the treasury and redistribute it to AAVE stakers and users, rather than simply accumulating this revenue in the treasury.

To further optimize the incentive mechanism and enhance the attractiveness of the GHO stablecoin, Aave also plans to introduce Anti-GHO as a new incentive mechanism for GHO, replacing the existing discount model. Anti-GHO is a non-transferable ERC20 token, and its issuance will be directly linked to the income generated by GHO.

At the launch of GHO, Aave utilized the Merit program to test a dividend incentive based on stability fee revenue, with an annual distribution scale reaching $12 million at one point. Today, the program has become self-sustaining, no longer requiring additional stablecoin funding support. This mechanism ties revenue and incentives together, not only enhancing AAVE staking rewards but also avoiding the "power shortage" flaw of a simple fee discount during bull-bear transition cycles.

The specific distribution mechanism is as follows:

1. GHO Fee Generates Anti-GHO: 50% of the GHO fee will be used to generate non-transferable Anti-GHO tokens.

2. The generated Anti-GHO tokens will be distributed in the following ratio: 80% allocated to StkAAVE holders (AAVE stakers), 20% allocated to StkBPT holders (Balancer pool stakers).

3. The original GHO fee discount will be discontinued, replaced by a profit-sharing mechanism based on protocol revenue.

Anti-GHO holders have two ways to use it:

1. 1:1 Burn to Offset GHO Debt: Holders can burn Anti-GHO at a 1:1 ratio to offset their GHO debt.

2. Convert to StkGHO: Holders can also choose to convert Anti-GHO to StkGHO to receive GHO staking rewards.

However, the implementation of Anti-GHO will require additional development and audit, or it will be formally activated in a subsequent "Aavenomics Part Two" proposal.

Initiating Buyback

In addition to revenue sharing, Aave also plans to launch an ambitious AAVE token buyback program. Over the next six months, Aave will allocate $1 million weekly towards repurchasing AAVE tokens, and this program will be overseen and executed by the newly formed Aave Finance Committee (AFC).

The AFC can execute buybacks directly or collaborate with market makers to buy AAVE from the secondary market. The repurchased tokens will be allocated to Aave's ecosystem reserve to support the long-term development of the ecosystem.

As the financial service provider for the Aave DAO, TokenLogic will plan the buyback strategy based on the protocol's overall budget, aiming to ultimately cover and surpass all AAVE-related expenses within the Aave ecosystem while maintaining prudent fund management.

With the expansion of Aave's new revenue streams by 2025, the AFC may propose an increase in the buyback budget. TokenLogic will adjust funding sources and strategies monthly based on the asset allocation of the Aave treasury.

Enhancing Protocol Operation Security and Efficiency

To further enhance the protocol's security and increase capital efficiency, Aave plans to introduce the "Umbrella" mechanism. Umbrella will integrate collateral and liquidity management to effectively mitigate default risks and liquidity crises. This is seen as a significant upgrade to the existing Safety Module.

The key advantages of the Umbrella mechanism include:

1. Robust Default Protection: Umbrella will provide Aave with a robust default protection mechanism, enhancing its resilience to market fluctuations and potential risks, especially in the backdrop of frequent hacks in the DeFi space.

2. Attracting Institutional Users: Umbrella's institutional-grade risk management capability will help attract more institutional users to participate in the Aave ecosystem, enhancing the protocol's on-chain asset management security.

3. Cross-Chain Deployment: The Umbrella system will be deployed across multiple blockchain networks such as Ethereum, Avalanche, Arbitrum, Base, and others, achieving broader applicability and higher security.

Furthermore, the Anti-GHO mechanism will also be integrated into Umbrella, making the repayment or conversion of GHO debt into interest-bearing StkGHO more straightforward and convenient. Aave currently faces a $27 million annual liquidity cost, and the introduction of the Umbrella mechanism will effectively enhance capital efficiency.

Lastly, the proposal also plans to complete the full retirement of the LEND token. LEND was Aave's original governance token before being upgraded to AAVE in 2020. Since 2020, the LEND token has been in a transitional period towards AAVE migration.

The proposal plans to finalize the retirement of the LEND token by freezing the LEND migration contract and reclaiming 320,000 unswapped AAVE tokens (currently valued at approximately $65 million). The proposal states that the community has had ample time to complete the token swaps, thus suggesting a formal closure of the migration process. The reclaimed funds will be allocated by Aave governance for specific purposes, such as ecosystem growth, security upgrades, or token burning.

This initiative will help address legacy issues in Aave governance, improving the protocol's operational efficiency. Additionally, unlocking these underutilized funds will further strengthen Aave's financial resilience, providing more abundant resources for its future development.

Next Blue Chip in Turbulent Times? How Does the Community View This Proposal

Currently, the proposal is still in the ARFC (Request For Comment) stage, and the community can discuss it on the Aave Governance Forum. The next step of the proposal will involve gathering community feedback and striving for consensus before proceeding to an offline Snapshot vote. If approved, the proposal will formally enter the on-chain governance proposal (AIP), and if successfully executed, buyback and other plans will commence in 2025.

Community members calculate that AAVE holders can potentially receive around a 3% annualized return through this proposal. Although the absolute numerical value may not seem outstanding, Aave has established its core position in the entire DeFi ecosystem, demonstrating traits akin to high-quality blue-chip stocks in traditional financial markets. With its robust operations, sustained growth, and clear revenue model, Aave has attracted the attention of more and more rational investors.

During an economic downturn, these types of assets typically have strong defensiveness, providing investors with relatively stable returns and a peace of mind holding experience. Of particular note is that as the global regulatory environment gradually relaxes and recognizes the DeFi sector, there is a possibility of reevaluating the value of DeFi assets. Therefore, redefining Aave as a "blue-chip" asset in the cryptocurrency market's new order carries ample rationale and forward-looking significance. It not only represents a conservative investment strategy but also heralds a certain trend in the future development of the DeFi sector.

Additionally, White House AI and cryptocurrency czar David Sacks has indicated a potential rollback of the so-called "DeFi Broker Rule" — the last-minute attack by the Biden administration on the crypto community.

The DeFi Broker Rule is a regulatory framework for decentralized finance (DeFi) intermediary service providers (such as trading platforms, lending protocols, etc.), aimed at ensuring compliance, user protection, and risk management. Core components include anti-money laundering (AML), know your customer (KYC), smart contract audits, fund security, and transparency requirements.

Reversing the DeFi Broker Rule means that DeFi protocols are not required to report and disclose customer information, easing the regulatory pressure on DeFi, which is also a positive development for Aave.

You may also like

Will MicroStrategy fall into a death spiral? What will the macro trend be in the second half of the year?

Morning Report | Illinois signs the strictest digital asset tax law in the U.S.; RWA tokenization market size surpasses $43 billion, institutions accelerate the migration of on-chain assets

Full version of the debut Q&A! Federal Reserve Chairman Waller: Sticking to the 2% inflation target, establishing five special working groups, individual did not submit the dot plot

From Disruptor to Shadow Market: The Crypto Market is Becoming a Colony of Traditional Finance

Dalio's important long article: How to position in the current market environment?

OKX Star analyzes Binance's competitive advantages: when regulation levels the playing field, competition has just begun

New gameplay for participating in initial offerings on cryptocurrency exchanges

Why Is Bitcoin Down Today? What the Hawkish FOMC Means for SpaceX, Gold and Nasdaq

DeepSeek Financing Story

Morning Report | DeepSeek completes over $7 billion in financing, with a valuation exceeding $50 billion; Musk's personal wealth has surpassed the total market value of Bitcoin

Cursor, why did you get on Musk's spaceship?

In the name of charity, for the benefit of the family: How the Trump family turned charity into profit?

Will Gold Break $4,500 After Tonight's Fed Decision? What XAUT and PAXG Traders Need to Know

SharpLink CEO: How to understand that Ethereum developers have just surpassed 1 million?

Morning Report | MiCA grace period expires on July 1; Kalshi's trading volume in the first week of the World Cup breaks $5.1 billion, setting a record

The foundation of SpaceX's trillion-dollar valuation: Who is dividing Musk's annual capital expenditure of tens of billions?

How to exit after asset tokenization?