Sonic DeFi Ecosystem Explosion: USDC Whale Entry, TVL Surges Against the Trend by 83%, How Much Further Can Token S Rise?

Original Title: "Sonic DeFi Ecosystem Explosion: USDC Whale Entry, TVL Soars Against the Trend by 83%, Can Token S Surge Again?"

Original Author: Lawrence, Mars Finance

Over the past tumultuous month in the crypto market, almost all mainstream chains' TVL has experienced a decline.

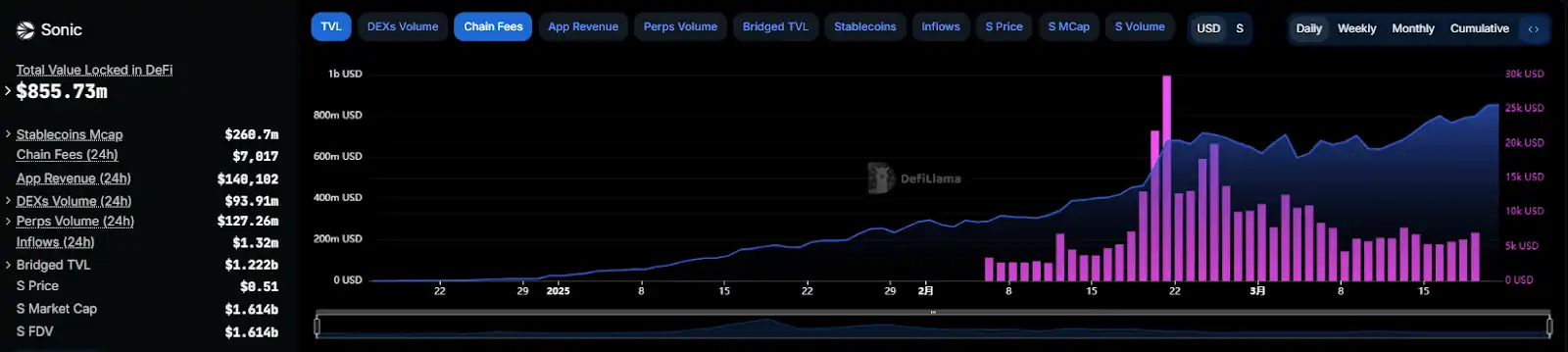

However, in this gloom, the Sonic Network has become a bright scenery, becoming the fastest-growing Layer1 public chain in terms of TVL due to its breakthrough growth. With Circle announcing the official deployment of native USDC and the cross-chain protocol CCTP V2 on Sonic, the network's TVL (Total Value Locked) has surpassed $854 million, with an astonishing increase of 83%. This leap, driven by technological innovation and capital support, is redefining the competitive landscape of Layer1 public chains.

Strategic Partnership: Circle's "Trust Vote" and On-Chain Prosperity

Native USDC and CCTP V2 cross-chain protocol are about to land on Sonic. This means:

· $10 Billion-Level Liquidity Injection: As the first high-performance chain to directly support native USDC, Sonic can accommodate Circle's ecosystem of over $28 billion in stablecoin reserves;

· Cross-Chain Efficiency Revolution: CCTP V2 will compress cross-chain asset transfer time from an average of 15 minutes to within 2 minutes, reducing Gas costs by 76%;

· Compliance Upgrade: USDC's institutional-grade audit and compliance framework pave the way for Sonic to expand into RWA, payment, and other scenarios.

Over the past month, Sonic's on-chain stablecoin reserves have grown from $100 million to $260 million, a surge of over 160%, with competitors such as DAI and FRAX seeing a 22 percentage point decrease, demonstrating strong whale recognition of the infrastructure upgrade.

TVL Soaring Against the Trend: The "Three Musketeers" Behind the 83% Growth

Over the past month and a half, while most public chains have been trapped in a TVL stagnation, Sonic has been absorbing funds at a daily average rate of $13 million. At the time of writing, Sonic's chain TVL has exceeded $850 million, ranking 12th on the Layer1 leaderboard. Its growth over the past month has exceeded 83%, leading all public chains.

Its growth momentum comes from three core protocols:

1. Silo Finance (Lending, TVL $1.94 Billion)

Adopting an isolated risk pool design, it supports overcollateralization of non-standard assets such as BTC and ETH. Its innovative "Dynamic Interest Rate Curve" ensures that the borrowing APY is always below the 30% liquidation threshold, with a default rate of only 0.17%, making it the top choice for institutional arbitrage.

2. Beets (Liquidity Staking, TVL $1.87 Billion)

It converts staked tokens S into interest-bearing assets stS, achieving a 23% annualized yield through an auto-compounding strategy. Users can further stake $stS in Aave V3, creating a "yield farming" model with an actual APY exceeding 35%.

3. Aave V3 (Lending, TVL $1.8 Billion)

On March 3, Aave deployed a lending market on Sonic, a high-performance blockchain evolved from Fantom. This marked Aave's first Layer 1 extension this year, signaling another step in its cross-chain expansion efforts. On the first day of launch, the supply limit was triggered. The Sonic Foundation and Aave DAO jointly provided $15.8 million in liquidity incentives, driving the USDC deposit APY to briefly surge to 19%, with a daily liquidation volume as low as $370,000, demonstrating better risk control than most competitors.

Sonic co-founder Andre Cronje (AC) also retweeted, stating that the current APY for the Sonic token S is 15.9%. If you invest $6.28 million today, you will earn $1 million in a year. This return far exceeds that of other Layer 1 token staking.

Furthermore, in just over a month, several DeFi protocol rookies have emerged on Sonic, with impressive data. Readers can also choose a project that suits them based on APY, risk, and other factors, achieving a decent stable return in the current turbulent crypto market.

Technological Breakthrough: Algorithmic Stablecoin Breakthrough and AC's "PTSD Paradox"

"We have cracked the algorithmic stablecoin puzzle, but past traumas make me hesitant." Sonic co-founder Andre Cronje (AC) threw out a shocking statement in a tweet on March 21. His team claimed to have solved the fatal flaws of predecessor projects like UST through a dynamic collateralization rate adjustment algorithm and a multi-level liquidation protection mechanism. Despite the significant technological breakthrough, AC still admits that the PTSD from the LUNA crash has not yet faded.

In response, DeFi researcher highonalpha said: "Not sure if it should be directly pegged to S, or pegged to a different protocol... Price pegging to S might be a good idea, but $UST and $USDN definitely have underlying trauma, and the blockchain is more important than the algorithm itself."

Others have also proposed the following solutions:

· Anti-Death Spiral Design: When the stablecoin uncouples, the system prioritizes burning governance tokens instead of minting more, avoiding liquidity dilution;

· Third-Order Interest Rate Model: Dynamically adjust borrowing rates based on collateralization rate, allowing APY to fluctuate elastically in the -5% to +25% range, suppressing speculative selling;

· Cross-Chain Breaker Mechanism: If the price deviates from $1 for more than 48 hours, trigger automatic cross-chain asset redemption to prevent systemic risk contagion.

The Sonic co-founder's contradictory mindset reflects the deep-seated dilemma of the algorithmic stablecoin race—algorithmic stablecoins do not have a perfect solution—and the $400 billion-level wealth evaporation caused by historical collapses like UST has made restoring market confidence far more challenging than achieving technological breakthroughs.

Capital Entry: Top Institutions' "Value Vote" and Valuation Game

In May 2024, Sonic completed a $10 million strategic funding round led by Hashed, with participation from SoftBank, Aave DAO, Bitkraft, and other institutions. This funding was precisely allocated to three major areas:

· Developer Incentive Pool: 30% allocated to DApp gas fee sharing subsidies, driving the number of ecosystem protocols from 62 to 312;

· Compliance Infrastructure: 40% invested in the Sonic Pay payment system, obtaining EU EMI licensing and Singapore MPI approval;

· Cross-Chain Security: 30% is allocated to the development of the Sonic Gateway's Fail-Safe mechanism, increasing the number of validating nodes from 7 to 21.

The current circulating market cap of $S is $1.6 billion, with a Market Cap/TVL ratio of only 1.9, putting it at a value proposition discount compared to mainstream Layer1 solutions. For comparison:

Looking at key metrics, Sonic has established a dual advantage in performance efficiency (TPS/Gas fees) and valuation rationality (Market Cap/TVL ratio):

· Capital Efficiency 306% Higher Than Solana: The market cap per $1 TVL is only 32.7% of Solana's;

· Healthier Staking Economy: A 62% staking rate higher than Sui and Aptos, with an annualized deflation rate of 1.8% forming the value support;

· Institutional Holdings Concentration: The top 10 addresses hold 39% of the circulating tokens, 17 percentage points higher than SUI, signaling strong market control.

"The value of $S is still significantly undervalued." Crypto fund UOB Ventures analyst Lucas Wong pointed out that if Sonic's TVL surpasses $2 billion within the year (150% annual growth rate), calculated at the industry average Market Cap/TVL ratio of 4, the token price could potentially hit $1, representing a 100% upside from the current $0.5.

Senior trader NihilusBTC stated that $S is breaking out of a descending wedge and once reversed, it could reach a price of $0.99.

Eve of Ecosystem Breakout: Where Is the Next Wealth Code?

On February 28, Pendle has officially launched on the Sonic Network, introducing the first set of liquidity pools in collaboration with Rings: stkscUSD (May 29, 2025) stkscETH (May 29, 2025). The Rings Protocol is an interest-earning stablecoin protocol where users can mint scUSD/scETH using various stablecoins or ETH assets. scUSD and scETH can be staked in the Veda Vault (becoming stkscUSD and stkscETH) and earn yield through blue-chip DeFi protocols like Aave.

On March 19, the EVM transaction aggregator Enso announced in a post that the Sonic Network is now officially live. Enso Shortcuts is currently supporting the Royco market to earn Sonic rewards. Sonic has kicked off its Sonic Points Season 1, allocating a portion of its approximately 200 million S token airdrop to its ecosystem. Royco makes earning and comparing rewards easy, while Enso works behind the scenes on protocol integrations and deposit operations.

With top protocols like Pendle and Enso joining in, Sonic's DeFi LEGO has revealed a unique opportunity:

1. Yield Tokenization (Pendle × Rings)

By splitting the principal and yield of scUSD/scETH, users can lock in a 40%+ fixed APY or leverage bet on interest rate fluctuations. The first pool attracted $43 million in deposits within 24 hours of launch.

2. On-Chain Payments (Sonic Pay)

Supporting Apple/Google Pay for direct USDC spending, with only a 0.3% fee, 92% lower than Visa's cross-border rates. The average daily transaction volume from beta users surpassed 12,000.

3. Meme Craze (THC, GOGLZ)

Community tokens saw over a 200% weekly surge, with DEX trading volume share spiking to 37%, replicating the early wealth effect of the Solana ecosystem.

Investment Conclusion: The Undervalued Layer1 Alpha Opportunity

From a fundamental standpoint, Sonic has built a sustainable DeFi growth flywheel through a triple innovation of technical performance, economic model, and ecosystem incentives. Its current market cap/TVL ratio is in the base layer's bottom range, with a higher safety margin compared to SUI at a similar stage. If TVL surpasses $20 billion within the year (annual growth rate of 150%), the S token price could potentially reach the $2-3 range (corresponding to a market cap of $60-90 billion), echoing the market movement from August to December 2024, where the emerging public chain SUI surged from $0.46 to $5.36.

Investor Strategy Recommendation:

· Long-Term Holding: Allocate to S Spot and participate in staking (APY15.9%), capturing ecosystem growth dividends;

· Leverage Strategy: Amplify gains through Pendle minting yield tokens or Shadow's x(3,3) model;

· Risk Hedging: Pay attention to airdrop unlock schedules, utilizing contracts and other tools to mitigate short-term volatility.

Sonic's rise is not only a rebirth of the Fantom ecosystem but also a benchmark case of the "efficiency revolution" in the Layer1 competition. In the DeFi narrative resurgence of 2025, its valuation restructuring may become one of the core storylines of this cycle.

You may also like

Stablecoins Finally Find Real Returns: On-Chain Reinsurance Re Explained | Interview with Re Founder Karan Saroya

The AI gamble of mining companies: Valuations enter a phase of differentiation, and it's hard to turn the tide

A letter from Alliance to entrepreneurs: Written on the occasion of Cursor selling for 60 billion dollars

Will MicroStrategy fall into a death spiral? What will the macro trend be in the second half of the year?

Blockchain Capital Partner: The Core Secret of Arbitrage

STRC unanchored by 11%, can the perpetual motion machine of Strategy still operate?

Bitcoin Market Analysis 2026: Can BTC Reach $150K by Year-End?

Bitcoin ETF Outflows Hit a Record $4.4 Billion: What Are Traders Doing With Their Cash?

WEEX App Just Got Smarter – New Tabs for Faster Trades & Easy Asset Management

WEEX All-New Search Features: Find, Trade & Earn Faster Than Ever

Morning Report | Illinois signs the strictest digital asset tax law in the U.S.; RWA tokenization market size surpasses $43 billion, institutions accelerate the migration of on-chain assets

Full version of the debut Q&A! Federal Reserve Chairman Waller: Sticking to the 2% inflation target, establishing five special working groups, individual did not submit the dot plot

From Disruptor to Shadow Market: The Crypto Market is Becoming a Colony of Traditional Finance

Dalio's important long article: How to position in the current market environment?

OKX Star analyzes Binance's competitive advantages: when regulation levels the playing field, competition has just begun

New gameplay for participating in initial offerings on cryptocurrency exchanges

Why Is Bitcoin Down Today? What the Hawkish FOMC Means for SpaceX, Gold and Nasdaq